|

||||||||||||||||||||||||

I love this discussion about $GME. blows my mind that this pro-level discourse is happening on X, for free, for anyone who is curious to see. incredible.

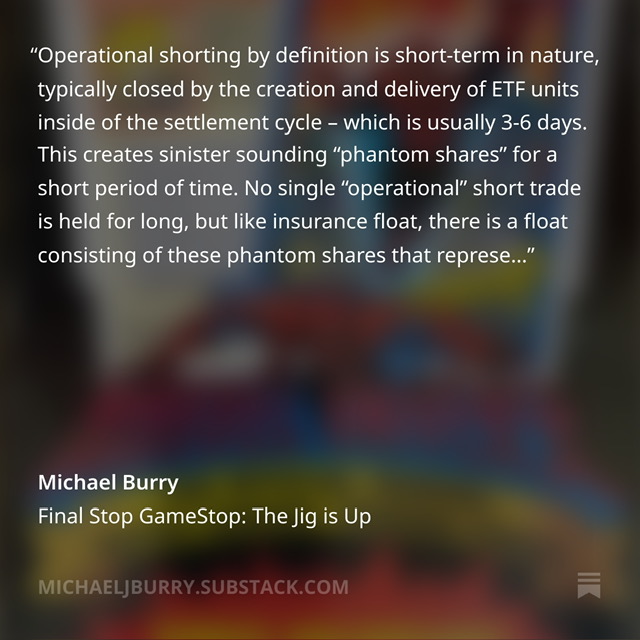

@michaeljburry I was happy to read that you made the connection between operational shorting and the use of creation and redemption privileges within ETF units.

I completely understand your explanation about shares sold short, short volume and market maker liquidity creation and I hope that I can ask a question to further pick your brain: what are your thoughts that this is merely the surface layer of a deeper problem? while I understand your explanation of a “phantom share” and the short-term nature of this dynamic as you describe it, what do you think about the repetitive and ongoing misuse of Reg SHO exemptions that allow the creation of persistent fail to delivers, *particularly* among ETF assets?

publicly-released data often shows outlier quantity of ETF fails on the *exact day* that an underlying equity would face forced delivery pursuant to Reg SHO Rule 204. do you find that curious?

of particular interest, with the popularization of single-equity leveraged ETFs marketed as leveraged exposure, there have been countless examples of outlier failure to deliver on the first trading day of these instruments, or again at deadlines to meet obligations on fails of the underlying common equity. worse yet, you can follow the data to daisy-chain and connect juggling of these obligations from one ETF to another, on the exact day of forced buy-in. some ETF products compound this situation by offering unlimited creation rights to their authorized participants, allowing for near-limitless access to an underlying security without raising the cost-to-borrow and reducing real demand on the open market. could you share your thoughts on this?

I and many others have observed this across many equities and I am not suggesting that this is an isolated issue targeted at $GME, having seen large FTD spikes on ETF vehicles for $MSTR, $TSLA, $NVDA, $CRWV, etc. it is as you say across many stocks and I wonder if you would agree that this is endemic within ETF products?

further, combined with the nature of continuous net settlement, I and many believe that this allows for the even-further deferral of delivery obligations which naturally, in a fair and efficient market, fundamentally impacts supply and demand and therefore price discovery.

I find it fascinating that many of the recent short squeezes like $SMCI, $CVNA, $MSTR will begin during pre-market hours, which happens to overlap with the CNS position report before the day cycle (T+1) begins, after the previous eve’s night cycle has batched orders. I can’t help but be intrigued if this is not attributable to lack of liquidity in premarket, nor dismissed as a coincidence?

I further question if this creates the potential for an environment with alignment of interests between authorized participants and issuers of these ETFs that would be in contrast with price discovery.

please accept my gratitude for sharing your professional, qualified perspective for everyone’s benefit and the time you take to provide explanations on market making and operational shorting specifically. I think this discussion is very valuable but went off-track when the subject of “legality” was brought up. at this point any serious retail investor should understand that the system exists by design with many shortfalls in the law such as “like-kind” and “reasonable expectations, prior to the entry of a short sale order, that sufficient securities will be available..” to ensure there is enough grey area to prevent “blatantly illegal” practices, at least most of the time.

I hope you can find the time to share your thoughts.

http://www.youtube.com/watch?v=QXIaNZi3mHQ

Duck9 is a credit score prep program that is like a Kaplan or Princeton Review test preparation service. We don't teach beating the SAT, but we do get you to a higher credit FICO score using secret methods that have gotten us on TV, Congress and newspaper articles. Say hi or check out some of our free resources before you pay for a thing. You can also text the CEO:

Duck9 is a credit score prep program that is like a Kaplan or Princeton Review test preparation service. We don't teach beating the SAT, but we do get you to a higher credit FICO score using secret methods that have gotten us on TV, Congress and newspaper articles. Say hi or check out some of our free resources before you pay for a thing. You can also text the CEO: