The 3-Component Fisher Stance: Critical Insights for U.S. Monetary Policy Stability (2000–2026)

By Larry Chiang, CEO Duck9.com and Founding Entrepreneur in Residence, Stanford University

The effective conduct of monetary policy stands as one of the most consequential responsibilities entrusted to the Federal Reserve.

In an era defined by rapid technological change, fiscal pressures, and global interdependence, understanding the precise stance of policy is not merely an academic exercise—it is vital to the economic security and prosperity of the United States.

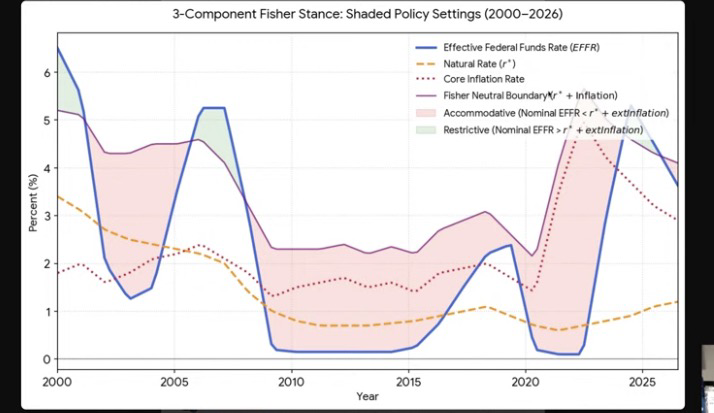

This chart, “3-Component Fisher Stance: Shaded Policy Settings (2000–2026),” provides a rigorous framework for this analysis by integrating the Effective Federal Funds Rate (EFFR), the natural rate of interest (r*), core inflation, and the Fisher neutral boundary (r* + inflation).

This chart, “3-Component Fisher Stance: Shaded Policy Settings (2000–2026),” provides a rigorous framework for this analysis by integrating the Effective Federal Funds Rate (EFFR), the natural rate of interest (r*), core inflation, and the Fisher neutral boundary (r* + inflation).

This visualization delineates periods when policy has been accommodative (nominal EFFR below the neutral boundary) versus restrictive (above it). Such clarity is essential.

Misjudging the stance whether too loose for too long or tightened prematurely can amplify business cycles, distort capital allocation, and erode the purchasing power that underpins American households and enterprises alike.

Core Components of the Fisher Framework

The Fisher equation, nominal interest rate ≈ real natural rate (r*) + expected inflation, forms the intellectual foundation. Here, the chart operationalizes it through three integrated elements:

• Effective Federal Funds Rate (EFFR): The actual policy instrument, reflecting the Fed’s direct influence over short-term borrowing costs.

• Natural Rate (r)*: The equilibrium real rate consistent with full employment and stable inflation, absent transitory shocks. Estimates of r* have trended lower over recent decades due to demographic shifts, productivity dynamics, and global savings gluts.

• Core Inflation: A measure stripping volatile food and energy components, offering a cleaner signal of underlying price pressures.

The shaded regions

pink for accommodative settings and green for restrictive highlight deviations from the neutral boundary. When the EFFR sits below r* + inflation, policy supports growth by encouraging borrowing and investment. When it exceeds this threshold, it exerts restraint to cool overheating or anchor expectations.

Historical Lessons from the Data (2000–2026)

Examining the two-decade span reveals recurring patterns with direct implications for policymakers and market participants:

The early 2000s and post-2008 period illustrate prolonged accommodative stances, with the EFFR held well below the neutral boundary amid recovery efforts. While necessary to combat deflationary risks and financial stress, extended loose policy contributed to asset price inflation and imbalances that later required correction.

The sharp tightening cycles, notably around 2004–2006 and post-2021, underscore the Fed’s determination to restore balance when inflation breached targets. The restrictive shaded area in the early 2020s reflects an aggressive response to pandemic-era supply shocks and fiscal expansion. By anchoring the EFFR above the Fisher neutral line, the central bank signaled commitment to price stability ~ cornerstone of long-term credibility.federal Reserve dot retard

Recent readings approaching 2026 suggest a complex transition. With core inflation moderating and r* estimates remaining subdued, the policy trajectory must navigate a narrow path: sufficient restraint to prevent reacceleration of prices, yet flexible enough to support sustainable expansion amid technological disruption and geopolitical uncertainties.

Why This Matters for American Competitiveness

Monetary policy is not conducted in isolation. Its stance influences credit availability for entrepreneurs, mortgage rates for families, investment decisions by corporations, and the dollar’s role as the world’s reserve currency. A miscalibrated stance risks:

• Eroding savings and fixed-income security for retirees.

• Distorting signals for productive capital allocation in innovation-driven sectors.

• Amplifying inequality if asset owners benefit disproportionately from loose conditions while wage earners face persistent inflation.

At Duck9, our work preparing consumers and businesses for robust credit environments has long emphasized the interplay between sound macroeconomic policy and individual financial health. A predictable, rules-based approach to the Fisher stance enhances the transmission of policy and supports the high-trust credit markets that power U.S. growth.

Forward Guidance and Policy Discipline

As we move through 2026, transparency around the three-component framework offers a superior lens for accountability. Rather than relying solely on headline EFFR movements, observers should track real-time deviations from the neutral boundary. This disciplined perspective guards against both complacency in low-rate environments and over-tightening that could unnecessarily constrain recovery.

The Federal Reserve’s dual mandate of maximum employment and price stability demands nothing less than rigorous, data-dependent calibration. The shaded policy settings in this chart serve as a timely reminder: sustained prosperity requires policy that neither overstays accommodation nor imposes undue restraint.

America’s economic preeminence depends on institutions that adapt while preserving core principles of stability and predictability. By internalizing the insights of the 3-Component Fisher Stance, policymakers, executives, and informed citizens can better navigate the challenges ahead; ensuring that monetary tools continue to serve the broader national interest.

Larry Chiang

Alum CEO, Duck9.com

VC Fund Of Founders

Stanford University EIR

650-283-8008

|

||

|

|

Duck9 is a credit score prep program that is like a Kaplan or Princeton Review test preparation service. We don't teach beating the SAT, but we do get you to a higher credit FICO score using secret methods that have gotten us on TV, Congress and newspaper articles. Say hi or check out some of our free resources before you pay for a thing. You can also text the CEO:

Duck9 is a credit score prep program that is like a Kaplan or Princeton Review test preparation service. We don't teach beating the SAT, but we do get you to a higher credit FICO score using secret methods that have gotten us on TV, Congress and newspaper articles. Say hi or check out some of our free resources before you pay for a thing. You can also text the CEO: